Gross Margin (%) = (Revenue – COGS) ÷ Revenue × 100

This formula look simple. But for platform seller, even the meaning of revenue now becoming complicated.

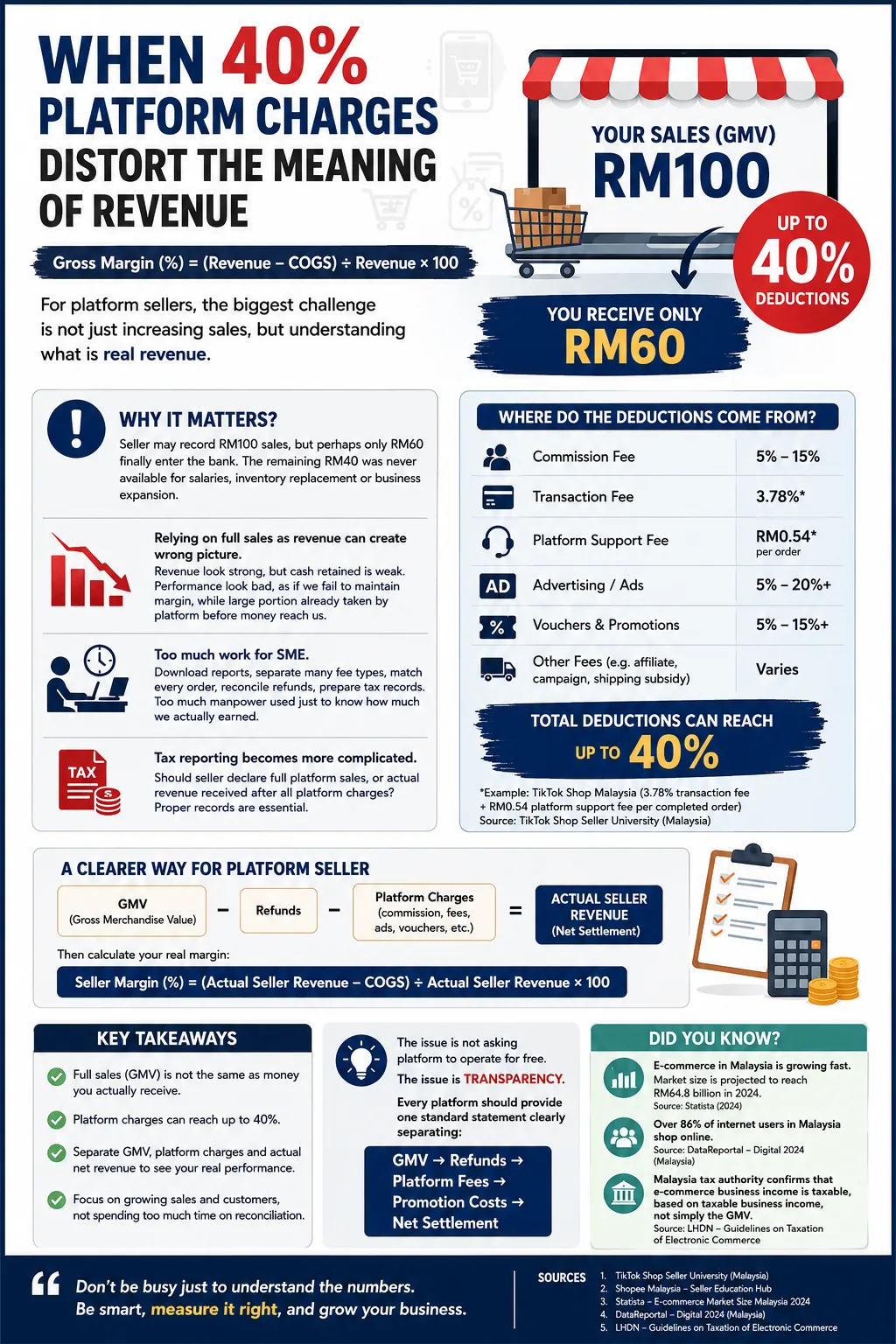

Platform seller may face several deductions: commission fee, transaction fee, platform support fee, affiliate commission, advertising, vouchers and seller-funded promotions. TikTok Shop Malaysia, for example, officially lists category-based commission, a 3.78% transaction fee and RM0.54 platform support fee per completed order. Shopee Malaysia also imposes commission, a 3.78% transaction fee and platform support fee. (TikTok Shop)

When everything stacked together, our actual deductions for certain sales or campaigns can approach 40%.

Seller may record RM100 sales, but perhaps only RM60 finally enter the bank. The remaining RM40 was never available for salaries, inventory replacement or business expansion.

Under IFRS 15, however, whether revenue should be reported gross or net depend on whether the business act as a principal or agent. A principal normally recognises gross revenue and records platform fees separately as expenses. An agent normally recognises only its fee or commission. Therefore, simply changing accounting revenue to the platform settlement amount may not always be technically correct. (IFRS Foundation)

But for SME management, relying only on gross sales can create wrong picture.

A seller may show strong revenue but very weak cash retained. Then seller performance look bad, as if we fail to maintain margin, while large portion already taken by platform before money reach us.

Perhaps SME need two separate measurements:

Accounting Revenue = Gross sales recognised under the applicable accounting treatment

Actual Seller Revenue = GMV – refunds – platform charges – seller-funded promotions

Then calculate an internal margin:

Seller Margin (%) = (Actual Seller Revenue – COGS) ÷ Actual Seller Revenue × 100

The pressure is not only margin.

SME must download settlement reports, separate many fee types, match every order, reconcile refunds and prepare proper tax records. Too much manpower used just to understand how much we actually earned, when SME supposed to focus on improving products and increasing sales.

Malaysia’s tax authority confirms that e-commerce business income is taxable, but tax is generally based on taxable business income—not simply the amount displayed as marketplace GMV. Proper records of income and related business expenses still required. (lampiran2.hasil.gov.my)

The issue is not asking platform to operate for free.

The issue is transparency.

Every platform should provide one standard statement clearly separating:

GMV → Refunds → Platform Fees → Promotion Costs → Net Settlement

Without this, SME may look successful based on sales figure, while the bank account telling a very different story.